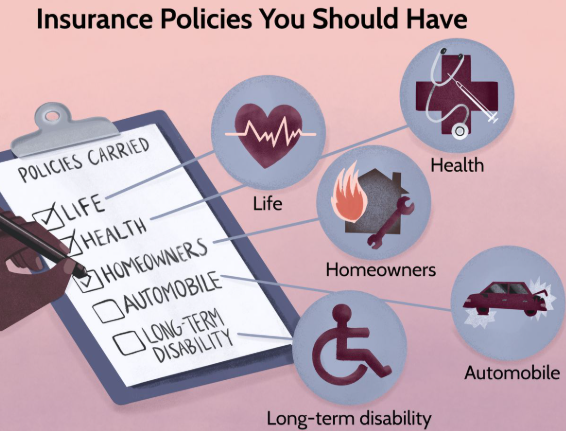

Insurance is one of those things most people know they should have—but don’t always fully understand until they really need it. And by then, it’s usually during a stressful moment: a hospital visit, a car accident, or a sudden loss in the family. That’s when insurance stops being an abstract monthly deduction and becomes something very real.

At its core, insurance is simple: you pay a smaller, regular amount to protect yourself from a much larger financial loss later. But the details? That’s where things get messy. Health, car, and life insurance each work differently, and understanding them can save you money, stress, and sometimes even your future financial stability.

Let’s break them down in a way that actually makes sense.

Health Insurance: Protecting Your Body and Your Wallet

Health insurance is probably the most talked about—and the most confusing. At its simplest, it helps cover medical costs so you don’t have to pay everything out of pocket when you’re sick or injured.

Think of it like this: your body is a high-maintenance vehicle. It doesn’t matter how careful you are; things can still go wrong. A broken arm, an unexpected infection, or something more serious can cost far more than most people can comfortably afford at once.

With health insurance, you usually pay a monthly fee (called a premium). In return, the insurance company agrees to cover part of your medical bills. But it’s not 100% coverage in most cases. You’ll often deal with:

- Deductibles: the amount you pay before insurance kicks in

- Co-pays: small fixed fees for doctor visits or prescriptions

- Co-insurance: a percentage of costs you share with the insurer

Here’s a relatable example: imagine you go to the hospital for a minor surgery that costs $2,000. If your deductible is $500, you pay that first. Then insurance covers most of the rest, and you might still pay a small percentage depending on your plan.

It can feel like a lot of moving parts, but the key idea is protection against catastrophic bills. Without health insurance, a single emergency can wipe out savings or push people into debt that takes years to recover from.

One common mistake people make is choosing the cheapest plan without looking at coverage. A low monthly premium might seem attractive until you realize you’ll pay heavily when you actually need care. Health insurance is one of those areas where “cheap” can become expensive very quickly.

Car Insurance: More Than Just a Legal Requirement

Car insurance often feels like something you buy just because the law says so. And while that’s partly true in many places, it’s actually much more than a legal checkbox—it’s financial protection against unpredictable road life.

Let’s be honest: driving is risky. Even the safest driver can’t control everything. Someone might hit your car while you’re parked. A sudden storm could damage it. Or you might accidentally cause an accident yourself.

Car insurance typically covers:

- Liability coverage: damage or injury you cause to others

- Collision coverage: damage to your own car after an accident

- Comprehensive coverage: non-accident damage like theft, fire, or weather

Here’s a simple scenario: you’re driving home and accidentally bump into another car at a junction. Without insurance, you might have to pay for repairs to both vehicles out of pocket. Depending on the damage, that could be hundreds or even thousands of dollars. With insurance, your policy steps in and absorbs most of the cost.

One way to think about car insurance is like a shared responsibility system. Everyone pays into a pool, and when accidents happen, that pool helps cover the costs. You’re essentially betting that you might need help someday—and paying ahead of time just in case.

But there’s a balance to strike. Some people over-insure older cars, paying for coverage that costs more than the car is worth. Others under-insure and regret it after a serious accident. The smart approach is matching coverage to your actual situation, not just picking random numbers.

Life Insurance: Planning for the People You Love

Life insurance is different from health and car insurance because you don’t benefit from it directly. That’s what makes it harder for some people to prioritize—but also why it matters deeply.

In simple terms, life insurance pays a lump sum of money to your chosen beneficiaries if you pass away. That money can help your family cover living expenses, debts, school fees, or anything else they need to stay financially stable.

There are two main types:

- Term life insurance: coverage for a specific period (like 10, 20, or 30 years)

- Whole life insurance: lifelong coverage that may also build cash value over time

Term life is usually cheaper and more straightforward. It’s often chosen by younger families who want protection during key financial years—like raising children or paying off a mortgage.

Here’s a real-world type of example: imagine a parent with two young kids and a home loan. If something happens to them unexpectedly, life insurance can help ensure the family doesn’t lose their home or struggle with daily expenses. It doesn’t replace the person, of course, but it provides financial breathing room during an incredibly difficult time.

One thing people often misunderstand is thinking life insurance is only for older adults. In reality, the earlier you get it, the cheaper it tends to be. And if someone depends on your income—even partially—it’s worth considering.

A useful way to think about life insurance is as a safety net for the people who rely on you. Not for you, but for them.

Why Insurance Actually Matters (Even When It Feels Boring)

It’s easy to see insurance as something you “have to pay for” without seeing immediate value. But that mindset changes quickly the moment something goes wrong. Insurance isn’t about expecting disaster—it’s about preparing for uncertainty.

Life has a habit of being unpredictable. Health problems don’t schedule appointments. Accidents don’t ask for permission. And financial stress tends to hit hardest when it’s unexpected.

Insurance smooths out those shocks. It doesn’t remove risk, but it makes risk manageable.

Conclusion: Peace of Mind Has a Price, but It’s Usually Worth It

At the end of the day, insurance is less about paperwork and more about protection. Health insurance protects your body and savings from medical shocks. Car insurance shields you from the financial chaos of road accidents. Life insurance ensures your loved ones aren’t left struggling if the worst happens.

None of it feels exciting. No one wakes up thrilled to review insurance policies. But that’s not really the point. Insurance is one of those quiet systems working in the background, waiting for the moment you need it most.

And when that moment comes, you’ll either be very glad you planned ahead—or wishing you had.

The smartest approach isn’t to overthink it endlessly, but to choose coverage that fits your life, your responsibilities, and your level of risk. Because in the long run, insurance isn’t just about money. It’s about stability, security, and the ability to recover when life doesn’t go according to plan.